TCAP - Problem we have a Houston

TCAP - Problem we have a Houston

Unpacking the FY23 Results

Dear reader,

It is with some satisfaction that contrary to speculation from many tipsters that Parameta would be put up for sale, the Oak Bloke felt this unlikely as the data was a key part to TCAP’s strategy. I asked:

Why would you want to break that virtuous circle and sell it?

Today we learn TCAP is planning an IPO with TP ICAP remaining the majority shareholder. My analysis of Parameta was that it is crucial to TCAP’s offering so selling off the crown jewels simply wouldn’t make strategic sense (even if it unlocked some value).

TP ICAP connects buyers and sellers in global financial, energy and commodities markets as a wholesale market intermediary, with a portfolio of businesses that provide broking services, data & analytics and market intelligence, with 60 offices across 28 countries, supporting brokers with award-winning and market-leading technology.

TP ICAP is a intermediary business plus a data/analytics provider which operates across:

“Global Broking” - via its 2 Tullett Prebon and ICAP brands

“E&C” - which is energy & commodities via its 3 Tullett Prebon, ICAP and PVM brands

“Liquidnet” division - an electronic trading network of US$33tn equity & fixed income assets - via 2 further brands Liquidnet and Coex

“Parameta” division is Data & Analytics - via its Parameta brand

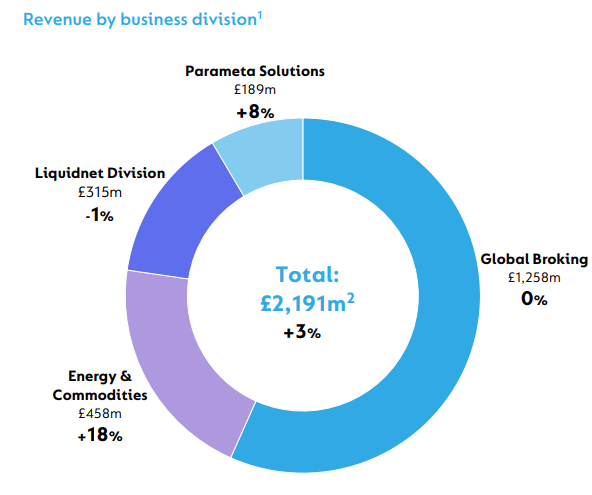

Reviewing the 2023 revenue we see growth in Parameta and E&C.

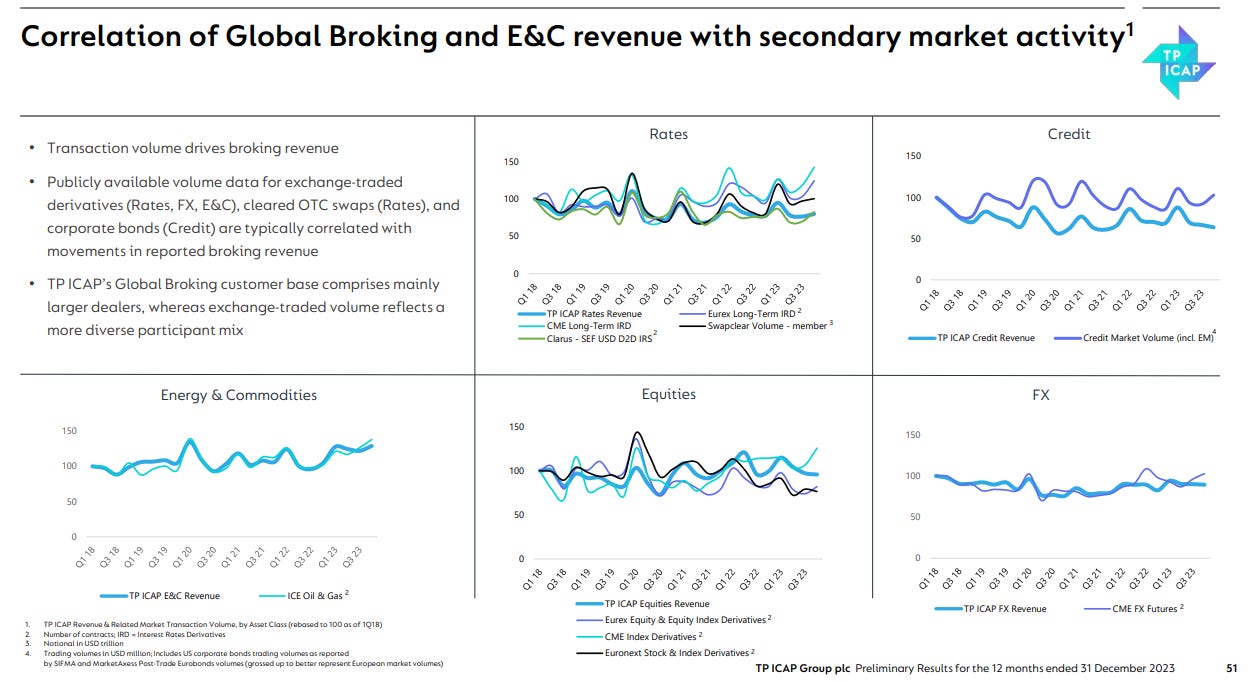

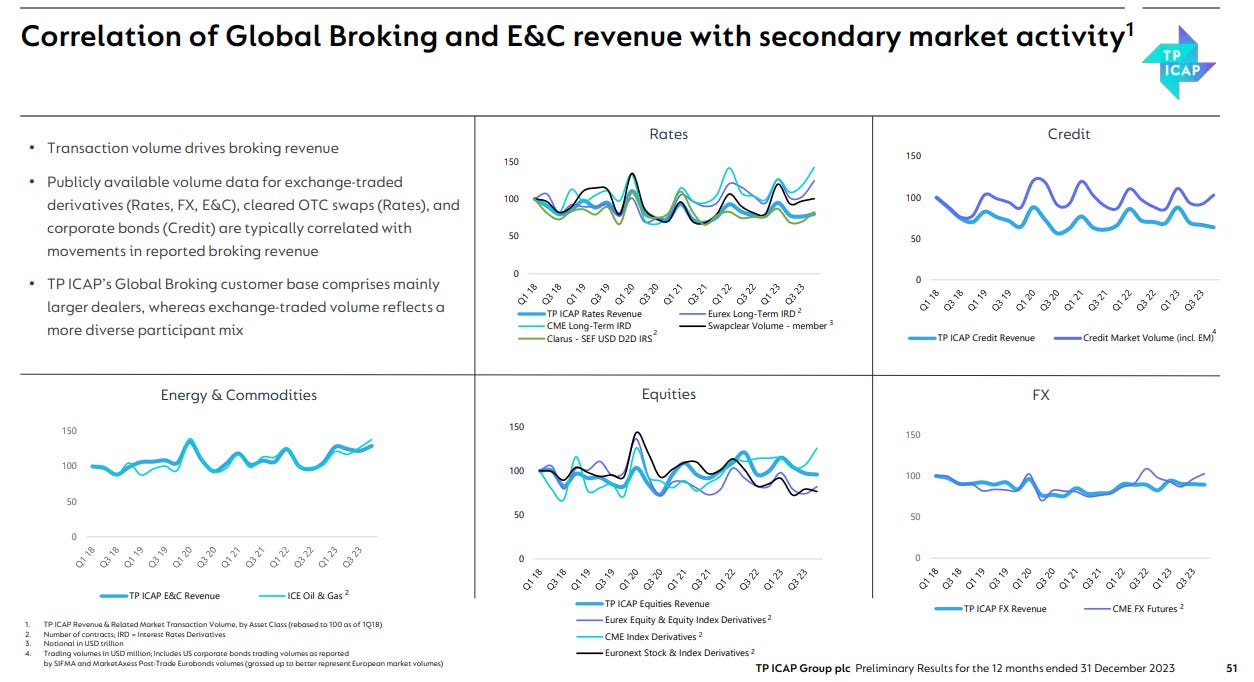

While half of revenue and contribution is via global broking which covers interest rate products so options, swaps and futures for bonds, treasuries, repo, municipals. Revenue is driven by activity. This chart illustrates the correlation.

Progress with “Fusion” has reached 44% of in-scope desks and 43 of the top 50 brokers are connected for transaction integration as well as accessing the whole family of TCAP products. Via Fusion you can connect to liquidity pools globally and buy and sell from the same single “award-winning” interface. As I previously explained in Introducing TCAP fusion feeds data and analytics to its Parameta division.

It’s not dissimilar to what Tesla have done with its ai tech - as Tesla drivers go about their lives the AI is learning from each driver - it has 200m miles experience as a result:

Liquidnet

More trouble from the “troubled” division. Paid too much some grumble. I don’t think so. TCAP needed to diversify. The drag has been due to Equity having two tough years but there’s room for optimism.

The £153m of “substantial items” (i.e. exceptions) are forecast to not repeat in 2024 (guidance is less than half - £65m)

A good chunk of that £153m is due to the reduction in block trading and this is partly driven by the simple fact many shares have a high unit price and a block is 10,000 shares or more! Maybe the definition will change.

A reduction in Liquidnet costs of £43m/year has been achieved during 2023 so we will see the fruits in 2024. It’s clearly the management and support cost being too high relative to the rest of the business where the lower profitabiarning lity lies.

The entire remaining goodwill and intangibles for Liquidnet is only £76m! - not much left to impair!

Liquidnet brokers grew contributions by 30% just the same as their E&C and GB colleagues in 2023.

Valuation

Apart from the dividend up by 19% (a 6.6% yield) and fully covered dividend being valuable, let’s look at whether 220p is good value?

£1.69bn market cap and 777.7m shares. 18% discount to NAV. Or 400% premium to TNAV of £350m (i.e. excluding goodwill). Also noting based on either a 3.5x P/FCF or 7x PE, this is cheap.

Continued execution of the strategy seems exactly the right course to take. Forecast earnings per share for 2024 are over 28p/share.

The Parameta spin out assuming that’s 49% forecast earnings of £100m-£105m in 2024 and a 20x-25x PE value means a £980m - £1286m valuation. That’s £1.26 - £1.66 a share upside. PE of at least 15X meanwhile “should” be a fair price for TCAP less the 49%. of Parameta (ie £240m - £49m = £191m x 15 = £2850m which is 68% ahead of £2.20 = £3.71.

That gets you to £4.97-£5.17 per share.

NB: You can read my past TCAP article here

This is not advice.

Oak

Hi OB, nice updated thoughts from you. Not invested here, although I want to be (not least because of my knowledge of the PVM business). Totally agree that that is a healthy yield to be receiving whilst waiting for the value to manifest into capital appreciation. For the patient, always a nice place to be.