TRR-rrrific!

Dear reader,

The nation loves its Royalty. Lots of gold, precious stones and a procession or too.

Many of the nation would be less familiar with royalties. Some companies like Trident specialise in those. The business model is I lend you some money and you repay me out of your revenues. Now that might sound risky but wait reader, there’s a key reason why money lending with mining might not. If you go bust, then usually debts die with the business. Creditors get X pence in the pound back, which might be zero. That’s the end of it.

With royalties the debt is on the land, on the resource. So if you go bust and let’s say Charles buys up the assets of your business his production is subject to the same royalty agreement. Of course, if Charles does something different like builds a palace over the mine then you’re stuffed, but typically the reason a mine gets bought is to continue mining. So the risk is diminished.

The next risk is the risk of mining itself. Costs can go up, the grade can be less than the sampling showed, the weather, strikes the list goes on and on. A royalty business couldn’t care less. Just like in Gold Rush where Tony Bleeps says how many ounces have you mined and holds out his hand for Parker to hand over a bag of gold, the costs of mining (for Tony) are irrelevant. Of course, what matters to Tony Bleeps is the more gold Parker mines the more royalties he gets so he will often say “Hey Parker have you thought about bleeping more bleeping XY and Z”. It’s the revenue that matters. Expansion is music to a royalty co’s ears, not a penny of cost but usually pounds of benefit

Another upside is simply that your royalty is over an area of land. If the production or if discoveries are made that are greater than expected that is of direct benefit to TRR. Paradox, for example, updated its reserves by 45% more lithium a few months back for example.

Now, mines can take years to develop and TRR finds itself waiting for a number of its Royalties to begin. In my prior article introducing Trident Royalties I explained how Trident offers a low(er) risk way to track commodities higher. If the price of gold goes up then the royalty typically goes up too (subject to any T&Cs you agree)

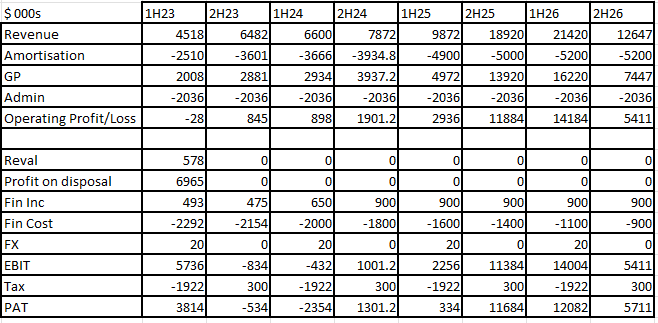

Of course there are costs for Trident. The cost of finance, or paying shareholders dividends are one. TRR expects to achieve a new $40m facility with lower rates which at maximum use would save $1.3m versus its current facility. There is also a depletion cost. As a mine is mined one must account for the proportion of depletion from the asset you hold. So for example I lend you $20m to fund a mine. Once that mine is 50% mined out (based on the reserves) then my asset (the loan) is only worth $10m.

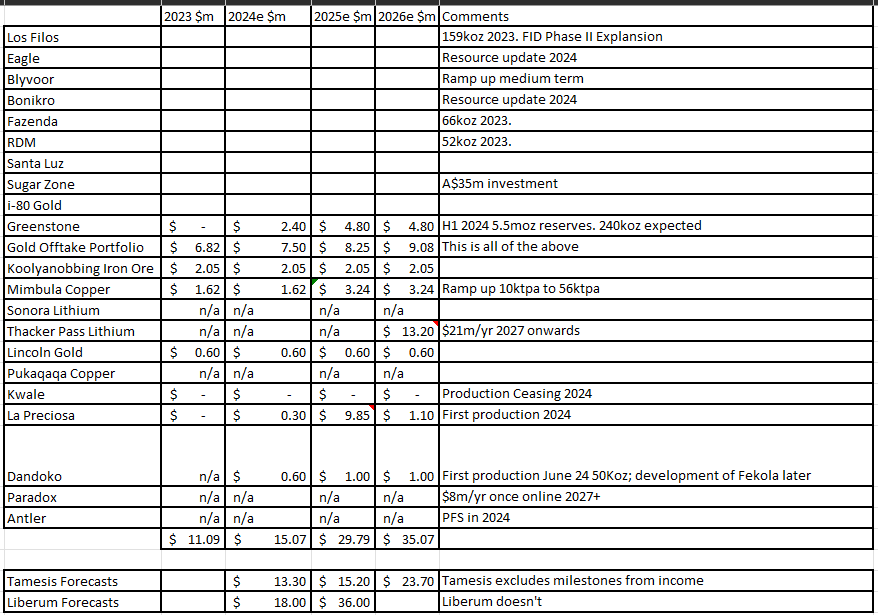

The below is what I’ve been able to piece together based upon the Royalty portfolio. Digging into the holdings it is apparent that:

a. There is quite a bit of expansion of existing mines

b. Progressive benefit as mines come on stream in 2024 and beyond

c. Resulting in progressive income just based on what’s already been put in place

d. In other words there’s room for upside from profitable disposals, from operators buying their way out of a royalty agreement, further royalties (i.e. there’s headroom for more deals)

Next of all I try to assign a royalty stream for each Royalty over the next years. The “Gold Offtake Portfolio” on row 11 comprises the first income for the first 9. This is based on $2k gold.

There are a lot of moving parts to TRR but relative to its share price it offers good value. The return is currently solely in the form of capital appreciation, and the aim of management is to grow the business in order to tap into cheaper finance, and larger projects. They are clearly already getting there.

That objective once met, one can see how in the future this could generate strong dividend returns for investors too.

This is not advice

Oak