Venture Life Group

Today’s results were a bit meh on the face of it. Was it a profit? Or a loss? Or both?

But dig a bit into the numbers and all sorts of interesting facts emerge:

Dentyl’s a write off? Or is it?

Dentyl was impaired due to poor sales by £0.4m.

I’ve previously written about Dentyl’s Cardiff University peer-reviewed research which gave evidence that CPC (the formula in Dentyl) can kill viruses which begin in the back of the throat. Viruses like Covid. This seems to have been lost in the ether. If Samarkand had any sense surely that’s a great inroad to the Chinese market?

I read this tidbit today. The 'bits' you see when you spit Dentyl mouthwash into the sink are not contained in the mouthwash itself; they come from your mouth. These bits are clusters of plaque bacteria that have been lifted from your teeth by the mouthwash's unique CPC formula, so you can see it working.

Reader, I had wondered about those bits! Now I know!

China’s a write off? Or is it?

I have no great insight but to say Samarkand had/has a good reputation for success in China so it is disappointing to hear they sold nothing. This remains an elusive future upside.

Input costs were herrendous?

It’s fair to say there was a cost of sale overhang in the H1 2023 results. H2 is looking better. FIFO costing means that as you rotate stock you pull through past spikes of cost into the P&L later on as you consume that stock.

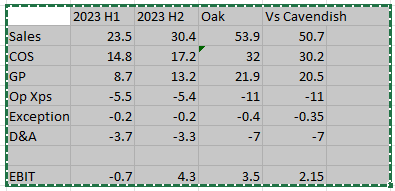

45/55

Historically the revenue split was 45% to 55% yet Cavendish believe full year will be revenue £50.7m which is far less than 55%. Why the drop? Especially when there are increased distribution agreements, numerous new product launches, launches of Amazon, and a bounce back of Pomi T all happening in H2? There was a 3% proforma increase H2 2022 to H1 2023 so I’m working with a 6% proforma for H2. Using a 45/55% split (£23.5m/45)*55 and a further 6%* uplift arrives to £30.4m revenue. If you compare 2022 H1 and H2 these also differed by that same proportion of £6-7m. Why would H2 only be £3.7m more this year per Cavendish?

*6% increase is conservative and is based on this comment in the H1 results:

“We see number of factors supporting our H2/23 forecast: -

- H2 weighting of the (higher margin) VLG Brand revenues

- Increased distribution points and the launch of newly developed products

- Order book strength, up c35% since the end of 2022A

- Management has taken action to support the gross margin, with the benefits of these expected to be seen in H2/23E

Assuming the same Gross Profit Margin as Cavendish’s estimate of 43.4% my numbers arrive at a higher GP (£21.9m) and EBIT (£3.5m) and therefore the 2023 outturn for net leverage I estimate as 0.8x-0.9x.

I don’t disagree with the valuation of 68p, particularly, but do think H2 will be stronger than forecast by Cavendish and regurgitated by the Investor’s Chronicle.