Dollar Strength, Bonds, and $CS $DB

Dollar Strength, Bonds, and $CS $DB

This week in Macro, even more intense than usual.

This week was packed with important market and geopolitical events that are seemingly pushing the world toward a global crisis. From the dollar rallying against all currencies, except the Russian rubble (!), to the UK debt and bond crisis that almost obliterated the UK pensions and forced BoE to an emergency intervention, to the sabotage of Noord Stream pipelines and Putin’s speech during the official annexation of 4 Ukrainian regions.

This week’s trending hashtags included WW3 (!), Putin, Lehman, Stock Market Crash, Pound, Credit Suisse, and Deutsche Bank.

And everyone’s new favorite phrase was the “Lehman Moment” as the currency and bond crises stole the headlines last week of September 2022, with the fall of the British pound, Credit Suisse and Deutsche stock prices dropping more than 95%, and European and global bond markets looking like they might soon follow suite.

So, let’s jump into the topics we promised to cover last time: the strength of the dollar and the widespread currency crises derailing the bond markets and potentially springing the Lehman-style defaults.

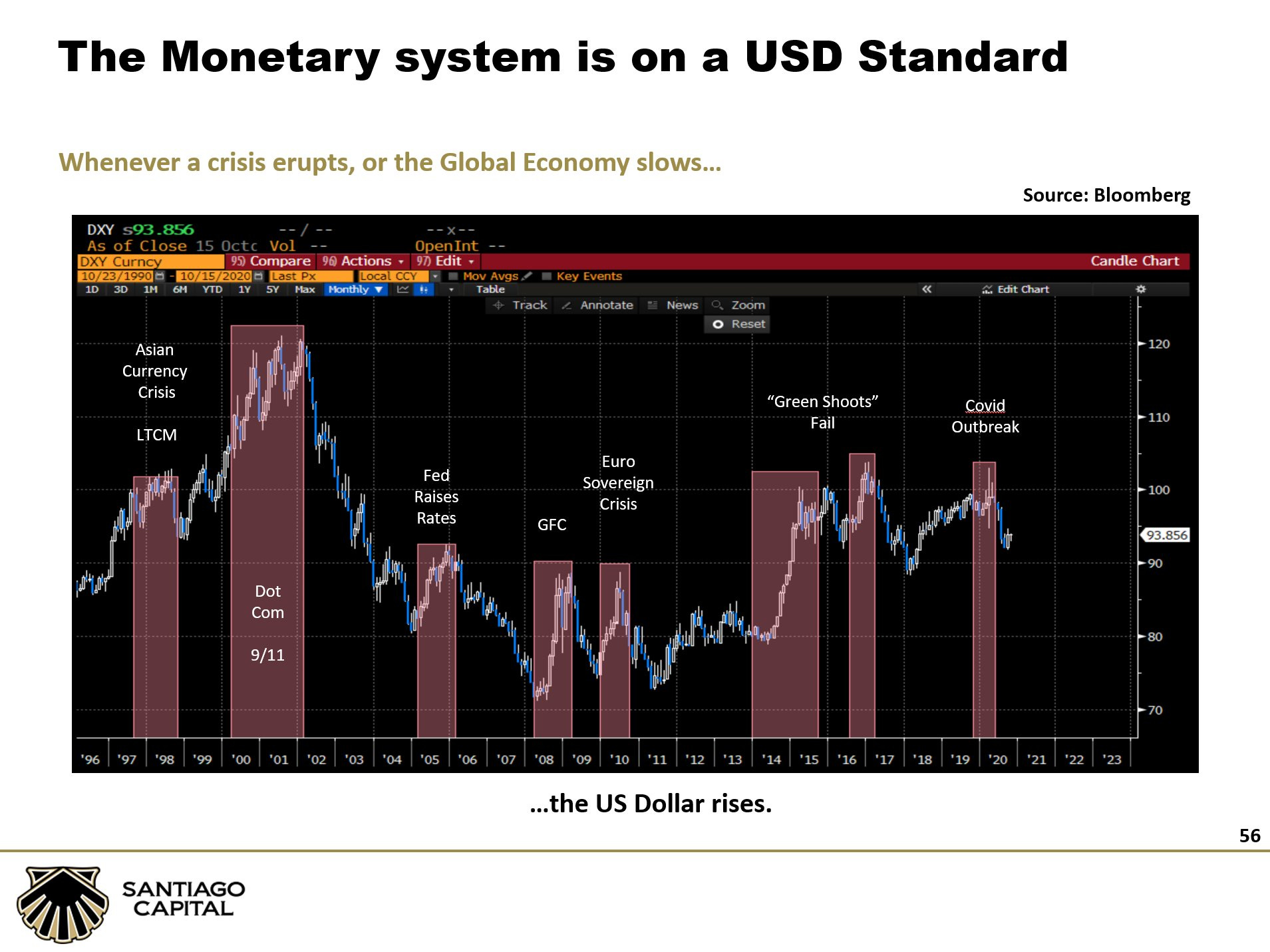

Dollar Strength

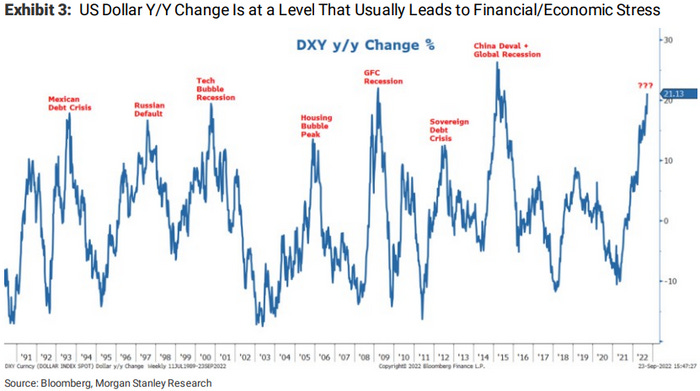

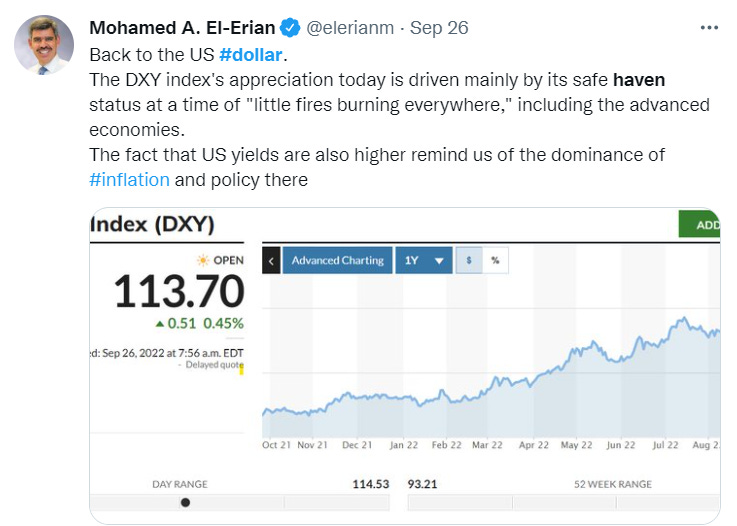

Early this week, the dollar index $DXY reached its highest level in over 20 years.

The USD has been rallying against other currencies for a while but picked up the pace between Sept 12 and 26, 2022.

The dollar’s strength was hailed as the economic strength by the white house.

It isn’t. Historically, a strong dollar coincided with every massive global crisis ($DXY reached 114.2 as of Sept 27, 2022, reaching the Dot Com levels).

The USD increases in price when the economies, institutions, and businesses around the world drive demand by stockpiling cash liquidity in the global reserve currency in fear of a major crisis.

A strong reserve currency stemmed worries about the currency crisis and its effects on other economies,

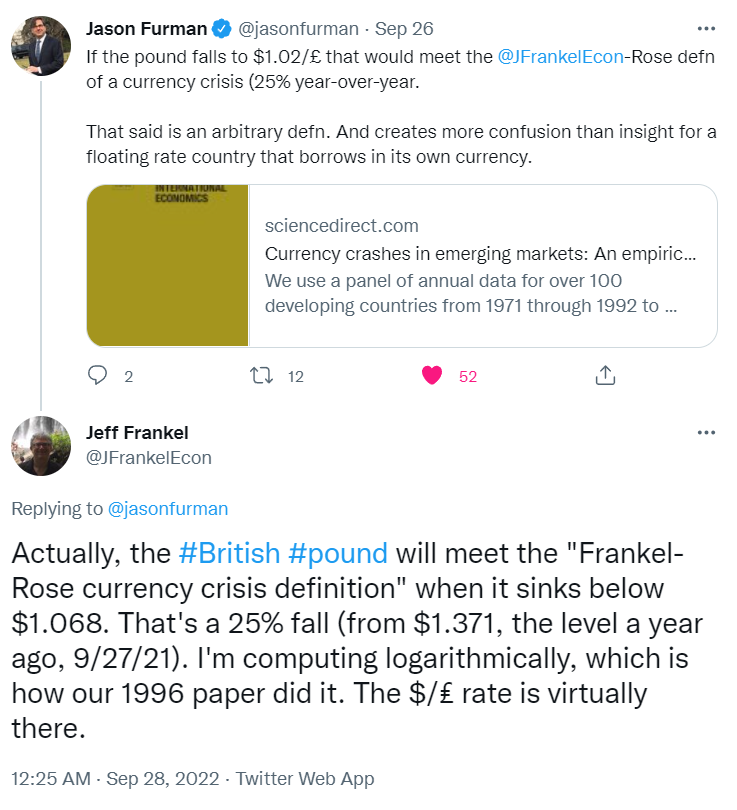

A currency crisis across other currencies (particularly the British pound),

*A currency crisis is described as a sudden, drastic deprecation of the currency followed by a loss of faith in the country’s economy and market volatility. It can force the authorities to raise domestic interest rates and sell foreign exchange reserves (FX reserves) to defend the currency. Currency crises cause wide-scale loss of capital and economic damage.

A liquidity crisis,

*A liquidity crisis is defined as a lack of cash or liquid assets across many businesses and financial institutions, which can lead to defaults and bankruptcies. The demand for liquidity abruptly increases while the supply drops as the markets for assets dry up and businesses can’t sell their stocks and bonds.

Or the related credit crisis.

*Credit crisis happens when there is a sudden disruption to cash movements across the economy, which affects banks’ and institutions’ ability to lend to businesses and each other.

On the bright side, the strong dollar helped the US export some of the local inflation onto other countries, which is great as long as they don’t trigger defaults and contagion across overleveraged indebted, and cross-exposed global banks and instructions.

*Contagion is the spread of an economic crisis from one market or region to another.

The UK Pound

The US rally against the pound was particularly severe this week, leading to near parity between USD and GBP.

And Pound weakened against the dollar after the Chancellor of Exchequer (The UK equivalent of the Minister of Finance), Kwasi Kwarteng, gave a fiscal statement to Parliament, Sept 23, 2022.

The Chancellor announced significant tax cuts and ‘growth’ policies, with the Treasury publishing The Growth Plan 2022, following his statement.

The pound also suffered an additional flash crash together with Euro after the Italy election results were announced (~2 AM local time, Sept 26). The Euro bounced back, but the pound didn’t recover.

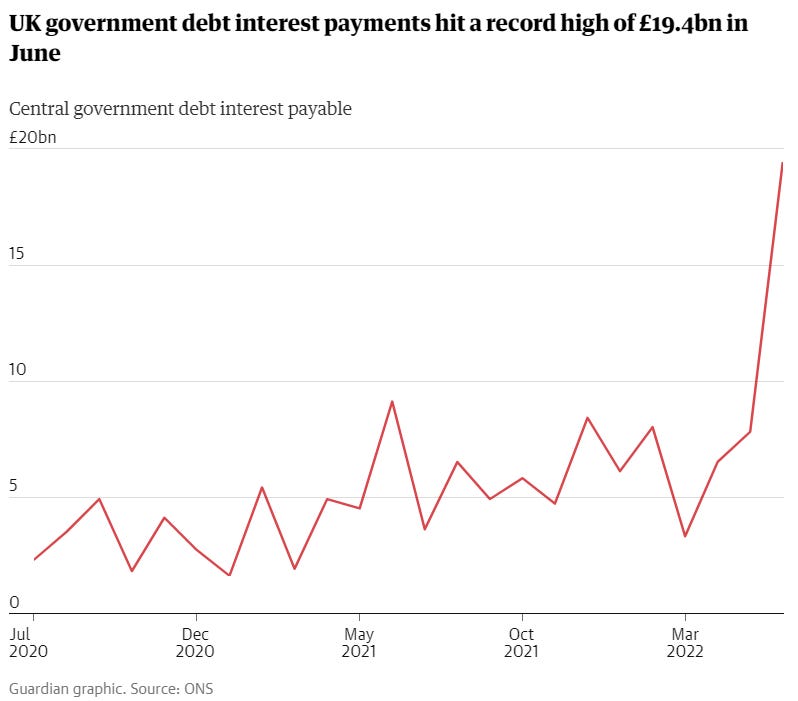

The controversial decision of the new British administration correlated with news of Great Britain’s skyrocketing debt servicing cost.

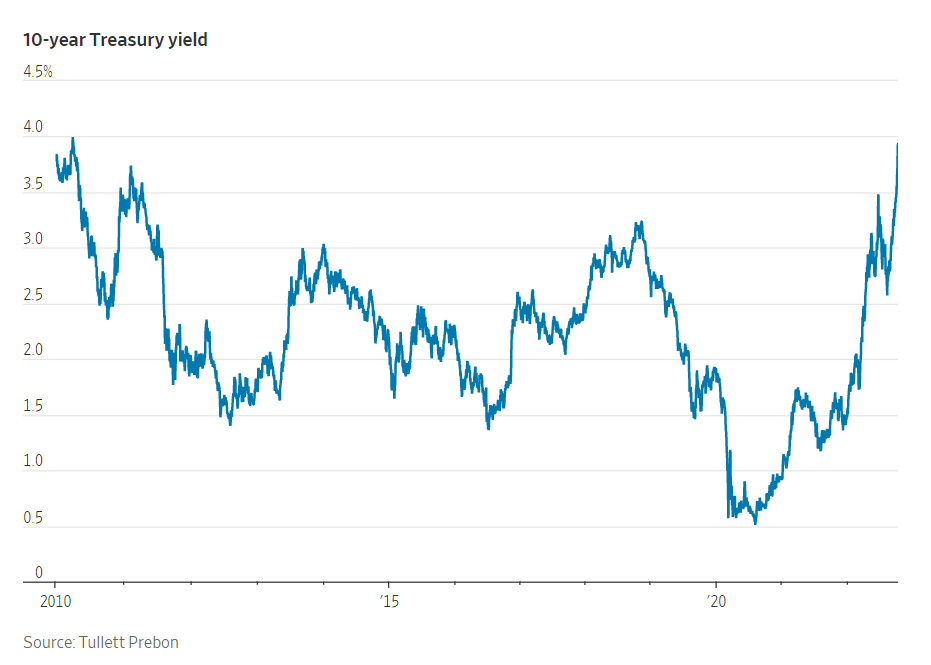

UK Bond Markets

UK Treasury bond yields increased to 10-year high while the prices and demand went down.

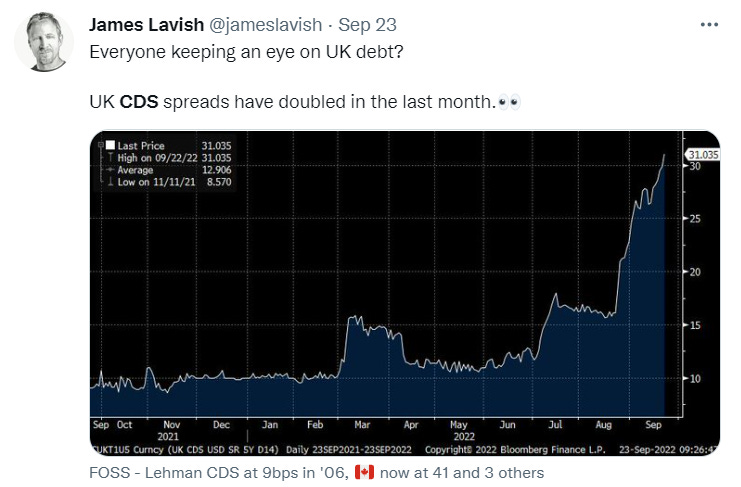

The UK bond crisis caused bond insurance in the form of the CDS (Credit Default Swaps) to get very expensive. CDS are held by many financial institutions, including pension funds.

The risk of mass defaults of the UK pension funds forced the Bank of England (BoE) to step in last minute

and stabilize the UK bond market, also called the UK Gilts.

Global Markets

The BoE decided to postpone a planned QT of £80bn and spend up to £65bn in ~2 weeks to directly purchase UK treasury bonds with a maturity of 20 years or more on the public market auctions.

The BoE move caused temporary US stock and bond rallies as the markets considered options that the other Central Banks would pivot in the near future.

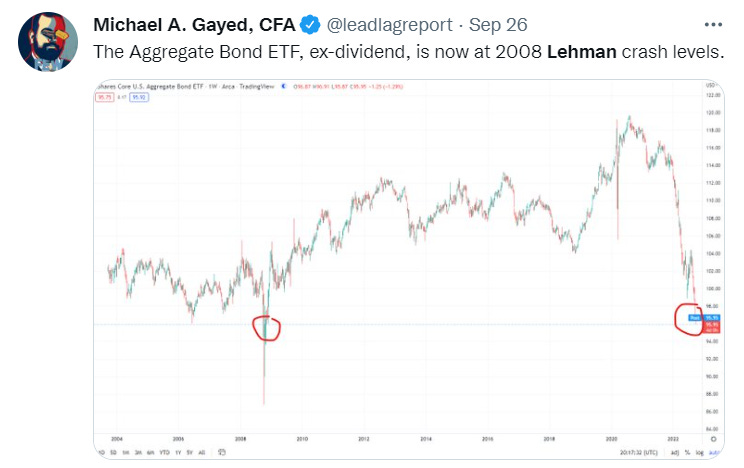

The rallies were short-lived and eventually added to another drop in the S&P500, Dow, and Nasdaq this week,

with the global bond market looking eerily similar to the 2008 crash levels.

Credit Suisse and Deutsche Bank

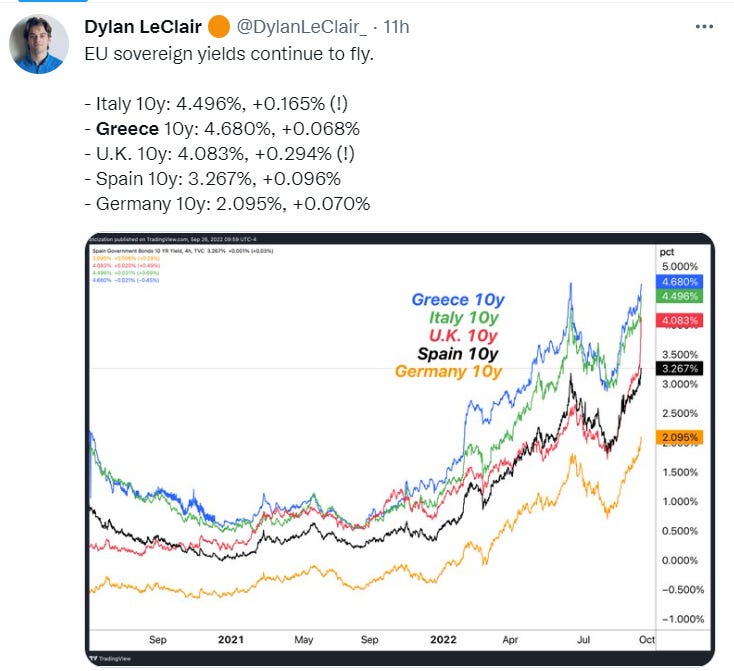

The dollar’s strength, the Fed’s tightening, high debt servicing costs, the European energy crisis, and finally the UK bond market collapse affected European and global bond markets and further eroded investor confidence in sovereign debts.

The cost of insurance of the treasury bonds, CDS (Credit Default Swaps), skyrocketed.

And the shares of the banks highly exposed to the CDS started tanking, led by Credit Suisse CB 0.00%↑ and Deutsche Bank DB 0.00%↑.

If any of them defaults, it could cause widespread contagion,

which is incredibly likely in the current debt-reliant, overleveraged system.

All will also depend on the Fed’s willingness and ability to continue providing liquidity through currency swap lines

and the record-shattering reverse repo loans that have been keeping financial institutions afloat for over 2 years.

In the next episodes we’ll discuss the other side of the ‘currency wars’ related to BRICS, OPEC, and other threats to the dollar’s reserve currency status that is wreaking havoc across economies but also keeping the US afloat.

Written by Natalia Nowakowska

Excellent update. Thanks!