Do you want your money or not? The story of the fictional income tax in the USA

Do you want your money or not? The story of the fictional income tax in the USA

Lies, lies, lies: they're going to get you!

OVER RECENT DECADES, state and federal tax agencies, with the occasional assistance of some courts, have engaged in a massive subterfuge for the purpose of successfully misapplying the income tax on an enormous scale The scheme has many facets, some more subtle and challenging to demonstrate or take in than others.

One of the simplest facets of the scheme to demonstrate is a systematic falsification of Supreme Court rulings on the subject of the income tax itself, and of the taxing clauses of the United States Constitution generally. This falsification involves outright lying-even in official documents and proceedings-about what has been expressly held by the high court on these subjects.

Understand, “falsification” as used here doesn't mean “misinterpretation”. The falsifications considered here involve actually ascribing to the court declarations which it not only did not make, but which it expressly rejected as false.

These falsifications have been created because what the Supreme Court DOES rule regarding the tax is inconvenient to modem government's desire for massive revenue They are used as pretexts for assuming authority to administer the income tax in ways contrary to its actual nature, for the benefit of government treasonists and those who control them.

WE'RE GOING TO LOOK at what the Supreme Court actually says about the nature and limits of the income tax. We're also going to look at falsifications of these holdings by both the US Internal Revenue Service and certain federal courts, at the reason these falsifications are 20 important to the revenue hungry government, and at the harm they have done Then we'll briefly look at the happier subject of events during the near decade-and-a-half since the overall subterfuge about the tax was first discovered and revealed.

The Truth

IN 1916, THE US SUPREME COURT laid out the meaning and effect of the 16th Amendment in a unanimous ruling in the case of Brushaber v Union Pacific Railroad Co. 240 US (1916). The Brushaber ruling, which remains the settled law-of-the-land today, unambiguously confines the income tax to the objects and administrative rules of an indirect excise tax only!

The Brushaber court holds that the sole purpose and effect of the 16th amendment is to undo and overrule its conclusion in Pollock v. Farmer's Loan & Trust, 158 U.S, 601 (1895) that a tax on otherwise excise-taxable dividends and rent becomes a property tax in those particular applications The Pollock court had reasoned that the linkage of dividends and rent to their personal property sources-the stock or the real estate from which they are derived transforms the income excise on those gains into a property tax on the sources, which therefore required apportionment in its imposition. The 16th Amendment, says the Brushaber court, severs (prohibits) the “source™ linkage imagined by the Pollock court. This overruling of Pollock allows the by then multi year-old income tax to be revived and to resume application as the excise tax it always has been.

THE BRUSHABER COURT VERY EXPRESSLY RULES that the 16th Amendment does NOT accomplish its task by creating some kind of hybrid tax which can have the character of a capitation of other direct tax and yet not be subject to the apportionment rule-a “non-apportioned direct tax”. This was, in fact, the exact contention of Frank Brushaber (against whom the court ruled), who reasoned from this faulty notion the confused conclusion that the post-amendment revival of the income tax created a Constitutional conflict. Here is what the unanimous Supreme Court says (among much else in this very Jong, thoughtful and comprehensive ruling): “We are of opinion, however, that the confusion is not inherent, but rather arises from the conclusion that the 16th Amendment provides for a hitherto unknown power of taxation, that is, at power to levy an income tax which, although direct, should not be subject to the regulation of apportionment applicable to all other direct taxes And the far-reaching effect of this erroneous assumption will be made clear by generalizing the many contentions advanced in argument to support it...”

Brushaber v. Union Pacific RR. Co., 240 US, (1916) the court goes on to point out that the very suggestion of a non-apportioned direct tax is completely coherent, because that would cause one provision of the Constitution [to] destroy another, that is, it would result in bringing the provisions of the Amendment [supposedly] exempting a direct tax from apportionment into irreconcilable conflict with the general requirement that all direct taxes be apportioned ... This result, instead of simplifying the situation and making clear the limitations on the taxing power, which obviously the Amendment must have been intended to accomplish, would create radical and destructive changes to our constitutional system and multiply confusion.”

“…. This ruling demonstrates its repeated pre-16th Amendment holdings that "taxation on income is its nature an excise, entitled to be enforced as such .”

PRETTY CLEAR, YES? The unanimous Brushaber court flatly holds that the income tax was, is, and remains an excise tax, and that the 16th Amendment in no way whatever authorizes a “non-apportioned direct tax"

Every possible authority agrees about what the Brushaber court says:

“The Sixteenth Amendment docs not permit a new class of a direct tax The Amendment. the [Supreme] court said. judged by the purpose for which it was passed. does sot treat income taxes as direct taxes but simply removed the ground which led to their being considered as such in the Pollock case, namely. the source of the income Therefore. they are again to be classified in the class of indirect taxes to which they by nature belong.”

Cornell Law Quarterly 1 Cornell L. Q. pp. 298, 301 (1915 to 1916)

“The Brushaber v. Union Pacific Railroad Case, Mr C J White, upholding the income tax imposed by the Tariff Act of 1913, construed the Amendment as a declaration that an income tax is “indirect,” rather than ... an exception to the rule that direct taxes must be apportioned “

Harvard Law Review, 29 Han. L. Rev. p. 536, (1915-1916)

“By the [Brushuber| ruling, it was settled that the provisions of the Sixteenth Amendment conferred no new power of taxation, but simply prohibited the previous complete and plenary power of income taxation possessed by Congress trom the beginning from being taken out of the category of indirect taxation to which it inherently belonged. and being placed in the category of direct taxation subject to apportionment by a consideration of the sources from which the income was derived - that is, by testing the tax not by what it was, a tax on income, but by a mistaken theory deduced from the origin or source of the income taxed ”

Stanton v. Baltic Mining Co., 240 US. 103 (1916)

“If [a] tax is a direct one, it shall be apportioned according the the census or enumeration If It is a duty, impost, or excise, it shall be uniform throughout the United States together, these classes include every form of tax appropriate to sovereignty” Cf Burnet v Brooks, 288U S 378, 288 U S 403, 288U S 405, Brushaber v. Union Pacific RR Co

Steward Machine Co versus collector of the revenue tax 301 US 548 (1937)

“The income tax ... is an excise tax with respect to certain activities and privileges which is measured by reference to the income which they produce The income is not the subject of the tax, it is the basis for determining the amount of tax”

“[T]he amendment made it possible to bring investment income within the scope of the general income-tax law, but did not change the character of the tax. It is still fundamentally an excise or duty...”

House Congressional Record, March 27, 1943. p. 2580. testimony of Former Treasury Department legislative draftsman F Morse Hubbard,

“The Supreme Court, in a decision written by Chief Justice White, first noted that the Sixteenth Amendment did not authorize any new type of tax, nor did it repeal or revoke the tax clauses of Article 1 of the Constitution, quoted above. Direct taxes were, notwithstanding the advent of the Sixteenth Amendment, still subject to the rule of apportionment “

Report No. 80-19A, ‘Some Constitutional Questions Regarding the Federal Income Tax Laws’ by Howard M Zaritsky, Legislative Attorney of the American Law Division of the Library of Congress

(1979)

"The sole purpose of the Sixteenth Amendment was to remove the apportionment requirement for whichever incomes were otherwise taxable. 45 Congressional Rec 2245-2246 (1910), at 2539, see also Brushaber v. Union Pacific R.R. Co. ., 240 US 1 240 US 17-18 (1916)"

South Carolina v. Baker, 485 U.S, (1988),

TO SUMMARIZE, THEN:

The Supreme Court's words in the Brushaber ruling itself,

*The 1916 Cornell Law Quarterly and Harvard Law Quarterly reporting on the Brushaber ruling;

*The Supreme Court, referencing and reiterating the Brushaber ruling, m 1916, 1937 and 1988;

*The Treasury Department's tax Legislation draftsman 1943 and the

*Library of Congress Legislative attorney in 1979 discussing the Brushaber ruling...

...all agree that Brushaber rules the income tax to always have been, and to still remain, an indirect excise tax; that the 16th Amendment does not originate the tax nor authorize any kind of nonapportioned direct tax; and that non-apportioned direct taxes remain Constitutionally prohibited.

The Lies

DESPITE THE UNIVERSAL CLARITY of what the Brushaber court says in what remains the settled law to this day regarding the meaning and effect of the 16th Amendment and the nature of the income tax, in 1980 a federal appellate court makes this bizarre and manifestly false pronouncement “[T]he income tax is a direct tax, See Brushaber v Union Pacific Railroad Co ,240 US 1, 19, 36 S Ct. 236, 242, 60 L Ed 493 (1916) (the purpose of the Sixteenth Amendment was to take the income tax “out of the class of excises, duties and imposts and place it in the class of direct taxes”).”

United States v_E 614 F.2d 617, 619 (8th Cir. 1980)

In 1984, another federal circuit court says this:

“The Supreme Court promptly determined in Brushaber v. Union Pacific RR. Co, 240 U.S 1, 36 236, 60 L Ed 493 (1916), that the sixteenth amendment provided the needed constitutional basis for the imposition of a direct non-apportioned income tax.”

Parker v Comm'r, 724 F.2d 469 (5th Cir CT. 1984) For decades the IRS has published and distributed in hard copy and, more recently, maintained on websites, as in this example.

Contention: The Sixteenth Amendment does not authorize a direct non-apportioned federal income tax on United States citizens.

Some assert that the Sixteenth Amendment does not authorize a direct non-apportioned income tax and thus, U.S. citizens and residents are not subject to federal income tax laws

The lies promulgated by our vaunted internal revenue service which is an illegitimate third party by the way:

The courts have both implicitly and explicitly recognized that the Sixteenth Amendment authorizes a non-apportioned direct income tax on United States citizens and that the federal tax laws as applied are valid In (ited States v. Collins, 920 F 2d 619, 629 (10th Cir 1990), cert, 500 US, 920 (1991), the court cited Brushaber v. Union Pac, RR, 240 US 1, 12-19 (1916), and noted that the US Supreme Court has recognized that the “Sixteenth Amendment authorizes a direct nonapportioned tax upon United States citizens throughout the nation ”

In fact, what is actually said by that Collins court cited by the mendacious IRS is even worse than what is quoted by the tax agency:

“For seventy-five years, the Supreme Court has recognized that the sixteenth amendment authorizes a direct nonapportioned tax , see Brushaber v. Union Pac, RR, 240 US , 12-19, 36 S Ct. 236, 239-42, 60 L Ed 493 (1916) ” United States v. Collins, 920 F 2d 619 (10th Cir. 1990)

These lies-by panels of actual US appellate court judges, in actual rulings by which actual Americans suffered actual and substantial harm-are grossly, egregiously and staggeringly criminal, and so glaringly false as to raise the specter of dementia This is the sort of behavior that should land these judges in prison, if not facilities for the criminally insane!!!

These lies are also fundamentally despotic in nature and purpose This fact is ironically underscored by the 1984 date of the Parker ruling quoted above ...Like the other judicial lies about Brushaber and its law-of-the-land ruling concerning the nature of the income tax and the ongoing Constitutional prohibition of any kind of non-apportioned direct tax, the Parker court's falsehoods seek to exploit a dynamic George Orwell insightfully explained in his book, 1984. "Who controls the past controls the future Who controls the present controls the past” The object to be noted that there is actually a compounded in the IRS assertion (one part is the repeat of the 1Oth Circuits falsehood about Brushaber ...the other is the incorporation of the expression, “cert denied" into that deceitful parroting) Contrary to what is mendaciously suggested by that inclusion, the Supreme Court's denial of certioria; in no way an affirmation of the circuit court's falsehood “It is elementary, of course, that a denial of a petition for certioria decides nothing many times".

of all the judicial lies is to enable the perpetuation of the “ignorance tax” scheme by corruptly falsifying history.

All told, the behavior exposed above is nothing less than subversion. These judges-and their present day mimics, co-conspirators and enablers-were and are oath-breaking enemies of the Constitution, engaged in a deliberate and sustained assault on the rule of law in America.

The Reason For The Lies AT THIS POINT YOU MUST BE WONDERING just what is going on. And you SHOULD be

wondering, because it's not pretty. But it IS pretty important. You see, excise taxes are privilege taxes.

As has been shown, the lies by some courts and by the tax agency are meant to hide the facts that the 16th Amendment DIDN'T authorize a non-apportioned direct tax and that, in concert with all other branches of government, the Supreme Court definitively holds that the income tax 1s an excise tax, The reason they don’t want YOU to know this is because excise taxes are privilege taxes, and CANNOT fall on “all that comes in”, or, in fact, on ANYTHING that comes in, if it doesn't proceed from the exercise of a privilege.

Of course, this sounds unbelievable. Needed proof will be shown 1n a moment, but first, think about this: If what I just said about excise taxes (or something just as significant in the same way) isn't true, why lie about the Brushaber ruling, the “non-apportioned direct tax” prohibition and the fact that the tax is an excise? Why say the tax exists because of authorization by the 16th Amendment, rather than acknowledge its 1862 origin, its administration for years before the Pollock decision interruption, and its mere resumption in 1913 as before, once Pollock was overruled by the amendment?

That is, if the rules or nature of an excise tax allow for the imposition of a tax the way you experience the income tax today, why try to hide or evade the fact that the Supreme Court says it’s an excise? And why lie about its date of origin, and about the Supreme Court flatly holding that non-apportioned direct taxes are forbidden?

If the fact that the tax is an excise DIDN'T somehow hinder the application of the tax in the way the revenue-hungry government wants to see it applied, there would be no lying. This is clear enough, isn't it?

"...Albert Gallatin, in his Sketch of the Finances of the United States, published in November, 1796, said. ‘The most generally rece:ved opinion, however, 1s that, by direct taxes in the constitution, those are meant which are raised on the capital or revenue of the people, ..'

"He then quotes from Smith's Wealth of Nations, and continues ‘The remarkable coincidence of the clause of the constitution with this passage in using the word ‘capitation’ as a generic expression, including the different species of direct taxes-an acceptation of the word peculiar, it ts believed, to Dr. Smith leaves litthe doubt that the framers of the one had the other in view at the tame, and that they, as well as he, by direct taxes, meant those paid directly from, and falling immediately on, the revenue..."

Pollock v. Farmer's Loan & Trust, 157 US 429 (1895)

Here is Adam Smith, the expert source relied upon by the Framers in their chosce of terms in the Constitutional taxation provisions, descnbing some of the tax applications and practices encompassed by “capitations” (which are also known as “poll taxes”, an expression which, in this context, has nothing to do with voting).

"The taxes which. it 1s intended, should fall indifferently upon every different species of revenue, are capitation taxes,"... “In the capitation which has been levied in France without any interruption since the beginning of the present century, ... people are rated according to .. what 1s supposed to be their fortune, by an assessment which varies from year to year" ... “In the first poll-tax [some] were assessed at three shillings in the pound of their supposed income,..."

Here is the definition of “capitations” from the official law dictionary of Congress when the income tax

was enacted in 1862:

"CAPITATION. A poll tax; an tmposition which 1s yearly laid on each person according to his estate and ability.“

Bouvier's Law Dictionary, 6th Ed. (1856) Capitations and other direct taxes must be apportioned

"No capitation, or other direct, Tax shall be laid, unless in Proportion to the Census or Enumeration herein before directed to be taken ”

United States Constitution, Article L. § 9, cl 4 ..and as shown, the 16th Amendment didn't change that fact Thus, we know by these legal facts also that the unapportioned income tax can't “fall indifferently upon every different species of revenue”, but instead can only concern distinguished revenue-which is to say, revenue proceeding from the exercise

of privilege, as in all excise taxes.

The Bottom Line

The receipts subject to the federal excise (the “income” in the federal income tax) are those produced through the exercise of certain federal privileges, and no others. Just like the name says, a federal income tax.

Now, can I get a big, SAY WHAT?!

... Cause, yes, you've been fooled, and lied to, and screwed-you and your parents and/or grandparents, for that matter, back to the early 1940s. That’s when the scheme all the lying is meant to conceal began in earnest. That scheme involves tricking Americans into legally characterizing all their payments and receipts as the subterfuge from exposure by obscuring the relevance of the privileged-unprivileged distinction.

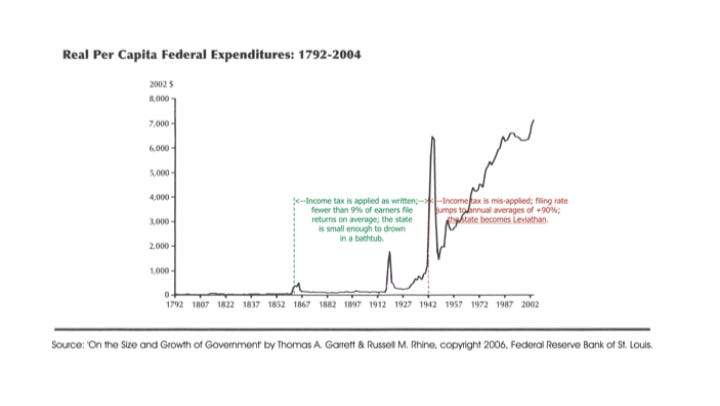

The effect of these lies and other crimes in facilitating the revenue and corresponding growth of the state

is dramatic, as vividly shown in this graph charting the growth of the federal government: see chart image

The book”Cracking the Code” — out since 2003, has really stirred things up!

Immediately upon publication of the book, readers began to recover amounts which had been improperly withheld or paid-in against potential tax liabilities they now realized did not arise. These folks learned what the income tax really falls on, and that in the past they had unwittingly participated in misapplying the tax to their own unprivileged earnings. Being serious, law-respecting American grownups, they promptly resolved, “No more!”

The recovered amounts include all normal federal, state and local income taxes, as well as Social security and Medicare taxes. (The latter are just “income surtaxes”.)

Educated Americans not involved in “withholding” situations have simply stopped falsely assessing themselves a tax and cutting checks to the various governments for amounts not actually owed under the income excise-their hard-earned money never leaves their own pockets in the first place.

All together, as best can be calculated, these now tens of thousands of American men and women have secured complete refunds of everything taken from them on more than two hundred thousand occasions, totaling more than $2 billion. Here are well over 1,000 documented examples of these victories in standing up for the law as actually written and overcoming the corrupt deceptions meant to enrich Leviathan in defiance of the Constitutional rules controlling taxation.

Lest we forget:

STARTING IN THE EARLY 1940s, the United States and many state governments stealthily launch a scheme to exploit what had by then become widespread public confusion about the nature of the tax (due to the diligent dis-information efforts of Progressives intent on implementing this scheme). The object of the scheme is the birth, care and feeding of an unrestrained Leviathan state, in defiance of the Constitution.

The scheme consists of two elements. The first is the nurturing of a myth that the 16th Amendment DOES authorize a direct tax (thus, one on "all that comes in", rather than only on privilege-related gains to which excise taxes are inherently confined) without the apportionment requirement.

The second element of the "ignorance tax" scheme is the establishment of a tax-related paperwork structure that induces people not involved in privilege-related activities to unknowingly mischaracterize their gains as though they are. This creates a legal pretext for collecting the income tax as the excise that it is, but where it does not objectively apply.

Between them the two elements of the scheme facilitate the wide and largely un-resisted misapplication of the tax, and that's just what was thoroughly underway by 1945. A river of wealth began flowing into Washington and about three dozen state capitals.

WITHIN TEN YEARS of the "ignorance tax" scheme being proven effective the remarkably clear and truth-revealing 1939 Internal Revenue Code is (otherwise inexplicably) replaced in its entirety as official evidence of the law by a 1954 version that is a masterful exercise in obfuscation. Within twenty-five years more, federal judges at the district and appellate court levels begin systematically lying about the Brushaber court ruling and the actual nature of the income tax.

And for those who for some bizarre reason don't want to follow what Peter had to say; let me refer you to the author by the name of Kenneth Royce he goes under the pen name Boston T. Party. His book is entitled ‘Goodbye April 15th’ it's about 35 years old and he only did one print -you can get it though used.

I have one more goodie for you from Steve Smith also known as ‘Red Green’ a TV show that ran in Canada for 15 seasons; 300 episodes total. With 85% of the viewers- USA viewers, so he tended to blend Canadian and USA things. Check out this clip see if it rings any bells now that you made it this far you're educated somewhat:

The author of the book “Cracking the Code” is Peter Eric Hendrickson he is also the owner of www.lostorizons.com

“Only a small proportion of the population of the United States is covered by the income tax. For 1936, taxable income tax returns filed represented only 3.9% of the population." Staff memo titled ' Collection at …Source of the Individual Normal Income Tax', Division of Tax Research, Treasury Department, 9 January, 1941.

The author is Peter Eric Hendrickson author of the book 'Cracking the Code' - owner of the website: www.lostorizons.com

Thank you so much for sharing this. I keep trying to find a way to get people to go to losthorizons.com and it’s so frustrating. You made my day.